Data Science and Risk Analysis in the Financial Banking

Leveraging advanced analytics to mitigate risks and drive informed decision-making in the financial landscape

Risk Analysis

Risk analysis is a process of assessing and evaluating potential risks and their impact on an organization, project, or decision-making. It involves identifying, analyzing, and prioritizing risks to make informed decisions on how to mitigate or manage them effectively.

Various products of the banking sector

The banking sector offers a wide range of products and services to meet the financial needs of individuals, businesses, and institutions. Here are some common products and services offered by banks:

Financial Risk Analysis

Financial risk analysis is specific to the evaluation and management of financial risks faced by organizations. It includes

- Assessing risks related to market fluctuations,

- Credit default,

- Liquidity,

- Interest rates,

- Foreign exchange, and

- Other financial factors.

Financial risk analysis often involves quantitative methods to estimate potential losses, calculate risk measures (such as Value at Risk), and develop risk mitigation strategies.

Types of risks analyzed in the financial banking sector

- credit risk: Credit risk refers to the potential for financial losses resulting from the failure of a borrower or counterparty to fulfill their financial obligations. It arises when borrowers or counterparties are unable to repay their loans or meet their contractual obligations. This risk can be mitigated through credit assessments, collateral requirements, diversification of credit exposures, and the use of credit derivatives.

Example: A bank lending money to individuals or businesses faces credit risk. If a borrower defaults on their loan payments, the bank may suffer financial losses. - market risk: Market risk arises from adverse changes in market conditions, such as fluctuations in stock prices, interest rates, foreign exchange rates, or commodity prices. It can lead to losses in the value of investments or portfolios. Market risk can be managed through diversification, hedging, and risk measurement techniques like VaR (Value at Risk) and stress testing.

Example: An investment fund holding a portfolio of stocks is exposed to market risk. If the stock prices decline due to market downturns, the fund’s value may decrease. - Liquidity risk: Liquidity risk refers to the potential difficulty of buying or selling an investment quickly and at a fair price without causing significant price changes. It arises from insufficient market liquidity or an inability to convert assets into cash when needed. Liquidity risk can be managed by maintaining adequate cash reserves, diversifying funding sources, and establishing contingency funding plans.

Example: A mutual fund holding illiquid assets, such as real estate or private equity, may face liquidity risk if investors want to redeem their shares, but the fund struggles to sell the underlying assets quickly. - Operational risk: Operational risk is the potential for losses resulting from inadequate or failed internal processes, systems, human errors, or external events. It encompasses risks related to technology, fraud, legal compliance, and business continuity. Operational risk can be mitigated through proper internal controls, staff training, disaster recovery plans, and risk monitoring.

Example: A cyber-attack on a financial institution’s systems that compromises customer data and disrupts operations represents operational risk. - Regulatory Risk: Regulatory risk arises from changes in laws, regulations, or government policies that impact the financial industry. It includes the risk of non-compliance with applicable regulations, which can lead to financial penalties, reputational damage, or restrictions on business activities. Regulatory risk can be managed through robust compliance programs, staying updated on regulatory changes, and engaging with regulatory authorities.

Example: A bank faces regulatory risk if new legislation imposes stricter capital requirements, necessitating adjustments to its operations and capital structure. - Reputational Risk: Reputational risk refers to the potential loss of reputation or public trust in an organization due to negative perceptions or events. It arises from actions, behaviors, or incidents that damage the public image or brand value. Reputational risk can be mitigated by maintaining high ethical standards, providing quality products/services, effective crisis management, and transparent communication with stakeholders.

Example: A scandal involving unethical practices in a financial institution can result in reputational risk, leading to customer loss, decreased investor confidence, and legal consequences.

Key steps involved in risk analysis in the financial sector

The process of risk analysis in the financial banking sector involves several key steps. While the specific approach may vary among institutions, here are the common steps typically followed in conducting risk analysis:

- Risk Identification

- Risk Assessment

- Risk Measurement and Quantification

- Risk Monitoring and Reporting

- Risk Mitigation and Management

- Risk Communication and Governance

- Regular Review and Update

- Risk reduction strategies

Risk Measurement

To identify risks monetary terms, here are some common measures for risk in the financial sector:

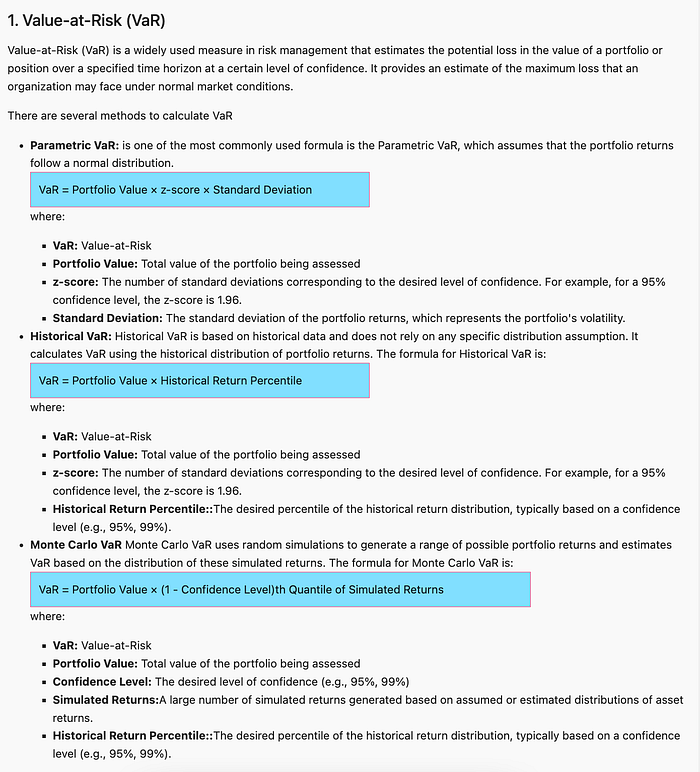

- Value-at-Risk (VaR): VaR is a widely used measure that estimates the potential loss in the value of a portfolio or position over a specified time horizon at a certain level of confidence. It provides an estimate of the maximum loss that an organization may face under normal market conditions. VaR is commonly used to measure market risk.

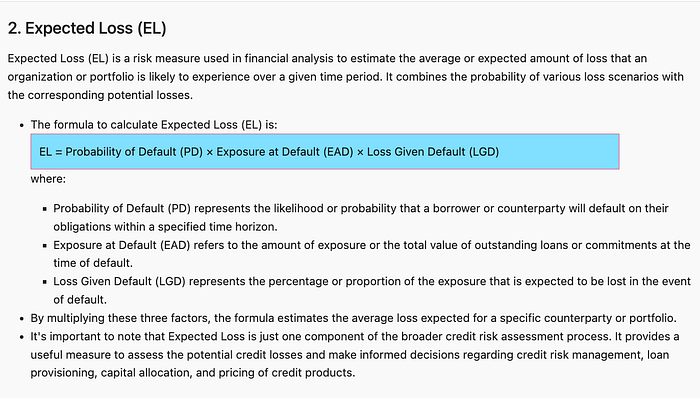

- Expected Loss (EL): Expected Loss is a measure that estimates the average loss that an organization is likely to experience from a particular risk. It considers both the probability of occurrence and the potential impact of the risk. Expected Loss is often used to assess credit risk.

- Conditional Value-at-Risk (CVaR): CVaR, also known as Expected Shortfall (ES), is a measure that provides an estimate of the expected loss beyond the VaR level. It quantifies the potential losses in the tail of the risk distribution, capturing the severity of extreme events. CVaR is useful for assessing risks associated with rare or extreme events.

- Risk-adjusted Return on Capital (RAROC): RAROC is a measure that evaluates the risk-adjusted profitability of an investment or business line. It considers the potential returns generated by the investment relative to the risks taken. RAROC helps in assessing the efficiency of capital allocation and supporting decision-making on resource allocation.

- Key Risk Indicators (KRIs): KRIs are specific metrics or indicators used to monitor and measure risks. They act as early warning signals by highlighting deviations from normal risk levels or thresholds. KRIs are tailored to specific risk types and provide ongoing monitoring of risks.

- Credit Ratings: Credit ratings assigned by credit rating agencies are measures of credit risk associated with financial instruments, such as corporate bonds, sovereign debt, or structured products. These ratings assess the creditworthiness and likelihood of default of the issuer, providing an indication of the credit risk involved.

- Loss Given Default (LGD): LGD is a measure that quantifies the potential loss a lender may face if a borrower defaults on a loan or credit obligation. It represents the portion of the exposure that is unlikely to be recovered in the event of default.

- Capital Adequacy Ratios: Capital adequacy ratios, such as the Basel III regulatory framework’s Common Equity Tier 1 (CET1) ratio, measure the financial institution’s capital reserves relative to its risk-weighted assets. These ratios help assess the organization’s ability to absorb losses and meet regulatory capital requirements.

- Operational Risk Indicators: Operational risk indicators measure risks associated with internal processes, systems, and people. They capture metrics such as the frequency of operational incidents, the time taken to resolve issues, or the level of compliance with internal controls. Operational risk indicators help monitor and manage operational risks.

- Stress Testing Results: Stress testing involves subjecting financial institutions’ portfolios and balance sheets to extreme scenarios or stress events. The results of stress tests provide insights into the potential impact of adverse events on the organization’s financial health and resilience.

Reference

- All details are available in my repository: https://github.com/arunp77/MonteCarlo-simulation

- The Jupyter notebook link from my repository: https://github.com/arunp77/MonteCarlo-simulation/tree/main/Finance-risk